Why Durable Medical Equipment?

Why Durable Medical Equipment?

Or "Another Sh*tty Thing in Healthcare"

The Durable Medical Equipment (DME) industry is not sexy. Why discuss the logistics of walkers and hospital beds, when telehealth is having its big moment, every other start-up pitch is a DTC pharmacy play, and companies like Everly Health and Ro have managed to build strong consumer health brands that weren’t conceivable 10 years ago? Sure, DME is not sexy. But it is so, so important to the quality of life of many senior and disabled Americans.

DME: A Primer

So what is Durable Medical Equipment? Per Medicare.gov, Durable Medical Equipment is (a) durable, (b) used for a medical reason, (c) not usually useful to someone who isn’t sick or injured, (d) used in your home, and (e) generally has an expected lifetime of more than three years. From my own research so far, I would segment these into 9 buckets (VERY open to feedback on better buckets with less numbering!).

(1) Manual Mobility: Relatively inexpensive equipment required for basic mobility around the house. Most people have seen the common examples: walkers, wheelchairs, crutches, and canes. Like most categories of DME, the costs can go up significantly when there is a medical need for customized equipment (not a lot of cost economics in custom-built).

(2) Electric Mobility: Powered mobility - used in cases where a patient’s movement and strength are so limited as to make manual mobility options unusable. Some of the most expensive DME available, which unsurprisingly has made it a target of largest fraud.

(3) Positioning: Similar to mobility, but more specific to movement within a concentrated space. Equipment in this category includes, but is not limited to, shower supports, toilet supports, and patient lifts (helping people stand up from a sitting position).

(4) Oxygen Based: Airflow assistance devices like CPAPs, BiPAPs, etc. Used for conditions like sleep apnea (difficulty in breathing during sleep) and general lung issues. These items can also be very expensive, and often require pre-authorization, sleep tests, and extensive documentation to be covered by insurance.

(5) Pressure relief mattresses: Mattresses specifically built for the purpose of relieving pressure and reducing risk of developing pressure ulcers. Interestingly enough, inpatient facilities are heavily incentivized to acquire these mattresses, as many states have rightly regulated hospitals based on the number of wounds developed during inpatient stays

(6) Recovery: Equipment used for the purpose of physical recovery, especially after acute surgery. This can include orthotics (specialized feet equipment), customized braces, and certain training equipment to help increase function over time. While standard braces are fairly inexpensive, labor and material costs can become substantial when custom-fitting is involved.

(7) Prosthetics: Like mobility devices, this area of DME is one that most laypeople are familiar with. Prosthetics are generally covered by insurance plans, however cosmetic prosthetics coverage is variable based on plan. Cosmetic prosthetics are those that are not for primary functional use, but rather to provide a life-life substitute for a loss body part, like a toe or finger.

(8) Pain Management: Medical devices to help with sufferers of constant pain, oftentimes by confusing the body’s pain receptors. NOT drugs like Oxycodone or Fentanyl.

(9) Bodily Function Management: Dialysis (equipment to supplant non-functioning kidneys), diabetes management and infusion pumps would fall under this category.

DME Documentation! A Paper Pusher’s Paradise

Like many things in healthcare, the question after “what is it?” is “who pays for it?” And again, like many things in healthcare, the answer is “your insurance company, but really very much you and your employer through insane premiums and deductibles :).” At the highest level, the coverage test is as follows: would this reasonably fit Medicare’s (a) - (e) definition of DME? Under this test, a wheelchair (with the right documentation) would likely be covered as DME, but a comfortable armchair that had medical benefit would not because someone without a medical condition would also find the armchair quite useful, thus failing to satisfy (c).

I’m broad stroking for brevity’s sake - the approval process is often much more complicated depending on the item and each particular plan’s policy. Various types of DME have all sorts of unique insurance hoops. For instance, a member must participate a sleep study to qualify for the use of a CPAP device to mitigate sleep apnea. Some types of equipment require month-long “test runs”, pre-authorization, re-authorization, or proof of failed, but less costly interventions. Some equipment won’t be covered under any circumstance - most inexplicably hearing aids, which still require a prescription and certainly satisfy (a) - (e) on the DME checklist.

These payor checks and balances are well intentioned, for the most part. After all, it is ostensibly the job of the payor to keep you healthy at the lowest cost reasonable and necessary. Further, billions of dollars of DME fraud has unfortunately necessitated extensive pre-checks and documentations for higher end equipment. The flip side of these payor requirements is a nigh unnavigable patchwork of different documentation needs and a long, painful process for patients to get the equipment they need, if they ever manage to get them at all. The sins of the few indeed…

DME is a massive, and growing, domestic market.

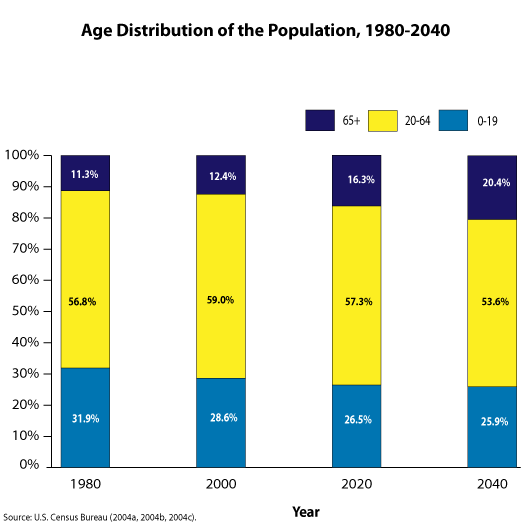

The domestic DME industry is a confusing, antiquated, and also massive. In 2019 alone, the United States spent $390B on care for the elderly and people with disabilities, according to a recent report by Melinda Gates’ Pivotal Ventures. This, compounded with an expected 25% (give or take by institute) increase in the 65+ demographic in the next 20 years, means that more Americans than ever are going to need reliable, affordable, and timely access to DME in the coming decades.

I am not the first person or group to notice this market and its inevitable growth. Those of the criminal persuasion did too - DME fraudsters were notoriously rampant in the 1990s and 2000s, putting insurance companies on the hook for billions of dollars of unnecessary (and in many cases, undelivered) DME. Not that this area of fraud has entirely died down - one particularly involved DME scheme allegedly defrauded Medicare of $1.2B, with 24 defendants indicted on related charges in 2019.

Private equity investors have also played a sizable hand in this space over the last decade or so. DME makes sense as a “platform play” (PE speak for an investible space) - take an old school, capital-intensive industry and roll up a bunch of successful regional/national players in different subsegments, then optimize for economies of scale across supply chain, customer bases, and regulatory burden. In fact, two of the largest public companies in DME, AdaptHealth and Apria, Inc., are the products of just such PE roll ups from well-know investment groups Deerfield and Blackstone.

Incumbent DME Suppliers are not cutting it- too small, too big, or just bad.

Bigger and better funded does not mean better. Let me introduce you to LinCare, a MASSIVE subsidiary of German conglomerate The Linde Group (not that there’s anything wrong with that). Lincare supplies all your oxygen needs - CPAPs, BiPAPs, you name it. Nice website, too. Now, let me introduce to 500+ LinCare customer reviews with an average rating of 1.12 out of 5. What’s the problem?

Big isn’t bad per se. As I’ll cover in a later piece, being an independent DME supplier in today’s regulatory climate is no walk in the park, and scale can help significantly overcome some of the hurdles. But Big AND Stupid is bad though, and just because companies like LinCare are regulatory compliant, doesn’t mean it’s OK for someone’s grandfather to wait 2+ months for a CPAP machine they need to sleep more than a few hours a night.

Despite this, a dearth of innovation

Despite DME’s sizable and growing US market cap, the sector’s innovation has been lacking to say the least. On first glance, this is especially puzzling given the adjacent explosion in venture capital funding and M&A surrounding home health. However, there are three factors that make the space in many ways incredibly unattractive for outside investors.

1) Capital Intensity - Contrary to popular belief, modern VCs do invest in businesses that aren’t B2B SaaS. However, the capital requirements of building in the DME industry are more well suited for traditional PE investment than they are for the typical VC investment. These ongoing costs include procurement, maintenance, repair, delivery, and customer service. When you factor in the high upfront and ongoing costs with #2 and #3 below - you can start to see why you basically haven’t seen venture touch this.

2) Regulatory Burden - An SVP of a large health system once did an analysis of whether to bring DME in house, given the pain and cost of dealing with DME suppliers. As a result of this analysis, the health system chose not to bring the cost center in-house, primarily due to excessive regulatory burden. When a health institution says something has too much paperwork, you know you have a problem. The various accreditations, re-accreditations, and the massive amount of documentation required to be a compliant DME supplier ha

3) Again, Who Pays (really)?

Burned by DME fraud for decades, payors across the spectrum have clamped down on what they will pay for, how they will pay for it (purchase v rent), and at what rates they will pay for it. Further, covered Medicare Part B expenses is a 20%/80% split between the member and their plan (less any remaining deductible of course). Without Medigap coverage, this 20% cost can still be quite sizable for members, and DME suppliers are often forced to sell these these remaining balances to collection agencies. From personal interviews and research, many of the remaining independent and small regional DMEs are opting to deal exclusively with higher income cash-pay clientele, citing margin-destroying rate cuts, bad debt expenses and overwhelming documentation requirements in their decisions. These factors have paved the way for oligopolies who have not earned their place through excellence of service or quality, but rather through the ability and capital to acquire they way to “victory”. More LinCares for all.

All hope is not lost though - there are some interesting start-ups in the space today. Founded by an Oscar Health alumnus, Series A start up Tomorrow Health is positioning itself as the e2e DME platform for DME suppliers, patients, providers, and payors - from streamlining patient intake for suppliers and providers, to customer service for patients and caretakers on insurance and DME navigation. With a stacked advisory board, a16z funding, and an early partnership with Geisinger, Tomorrow Health has built some promising early momentum. CO-based Health Sqyre is another interesting tech-enabled business here - taking a user-friendly marketplace approach specifically for sleep apnea related DME. Having played around with the website myself, I can say it is a delightful user experience lightyears ahead of many of the “XYZ.com” 2000s-like era DME websites of suppliers.

So What?

Ultimately, my goal is to move the needle a bit on where potential healthcare founders can focus their entrepreneurial juices on. Two spirited new players is not enough: we need more to right size a space that is highly fragmented, technologically behind (more so than other sectors), with opaque, low-quality incumbents. Hope you’re enjoyed this first piece - more to come!

Interested in learning more? Want to give feedback? Work at a SNF, DME supplier, hospice, or outpatient rehab facility? Let’s chat. Email me at ed.manzi55@gmail.com.