Competitive Bidding

Competitive Bidding

Why 40% of DME suppliers have left the industry...

Today, I’d like to talk a little bit about the biggest “disruptor” in the DME industry this decade - the Competitive Bidding Program (CBP). CBP has been Medicare’s primary response to reports of DME fraud and overspend - and as you’ll see below, the macro impact on the industry has been seismic. This isn’t the only tool in the playbook for reducing spend - prior auths, capped rentals, etc - but given the impact, we’ll focus on just CBP for this piece.

Some Legislative History

CBP was in the legislative woodworks since roughly the turn of the century. By that time, CMS was noticing that their DME reimbursement rates were far higher than those of commercial payors. Unlike these payors, CMS rates were often based off of manufacturer list prices. But, as any payor or provider will tell you, nobody pays close to a list price in healthcare (if you’re insured, that is). Thus, DMEs consistently made off with exorbitant margins, and CMS and taxpayers were stuck with the bill.

Needless to say, CMS had to do something about this - and thus Competitive Bidding was born. After some early pilots in 1998 and 2000, Congress mandated the development of a national program via the Medicare Prescription Drug, Improvement, and Modernization Act (MMA) of 2003. While the national launch was initially set for 2008, numerous implementation barriers held up the launch, and the program was finally launched nationally in 2011.

Program Mechanics and Roll Out

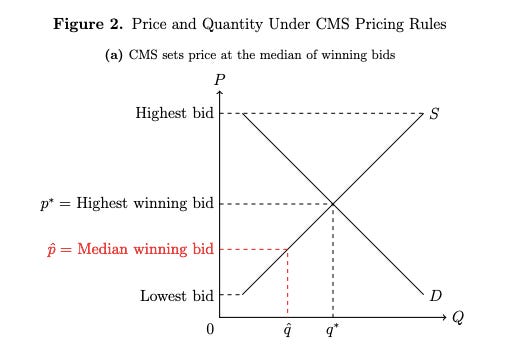

So what exactly was the Competitive Bidding Program, and how did it work? To illustrate, let’s use the example of Power Wheelchairs in LA County - a Metropolitan Statistical Area (MSA) . First, CMS requests bids for the entire product category of Power Wheelchairs in the MSA, which includes all types of power wheelchairs (bariatric, lightweight, etc) and relevant accessories. Medicare assigns weights (known prior to bid) to each category product by historical relative usage. Interested DME suppliers must submit bids for ALL the products within that category, and may not bid prices higher than the currently set administrative rates. Once all bids are submitted Medicare awards a number of exclusive, 3 year contracts to the lowest weighted price suppliers who meet solvency and quality standards. These contracts are set at the rates of the median accepted bid, meaning that half of the awarded suppliers receive a rate higher than their bid, and half receive a rate lower than their bid.

CMS followed a roll-out you would probably expect for a program like this - start small and grow in scope and number of products, focusing on the highest cost burden products first. In 2011, CBP was introduced to 9 MSAs in 6 product categories (231 products), dubbed the Round 1 area. In 2013, CBP was expanded to another 91 MSAs for 8 product categories (196 products), dubbed the Round 2 area. Thirdly, CBP set up a National Mail-Order competition specifically for diabetic supplies in 2013. Every three years, the contracts from the last round expire and a re-contract period ensues. For instance, Round 1 executed re-compete bids & contracts starting in 2014 and 2017, while Round 2 and the National Mail Order program executed similar re-compete bid & contracts in 2017. Each re-compete round start with another bidding process, followed then by an awarding process, while also expanding and refining the product list to be negotiated on.

Program Issues

CBP had some major flaws with downstream macro implications (hindsight is 20/20, acknowledged). The largest issue was setting the contracted rates at the median accepted bid price. Any rational economist could tell you that offering a supplier less than their perceived value is likely to push them out of the market. While CMS intentionally awarded a surplus of contracts to account for a percentage of drop-out, this surplus was certainly not 50% more. Yunan Ji’s working paper on DME has an excellent graph detailing this economically.

Another CBP issue is the non-binding natures of the bids. Ironically, the non-binding nature of bids was decided on to protect the awarded bidders who were above the median bid line who wished to opt out. One CMS-created problem begets another CMS-created problem, it seems. The more pernicious side-effect was that suppliers on the lower end of the bid spectrum could also pass on their awarded contracts, which meant that suppliers could put in bids that didn’t appropriately factor in their operating & admin costs and opt out later if that turned out to be the case - reducing expected supply

The third flaw in CBP’s design was the use of weighted items per product category - incentivizing bidders to game the system. How? I think economists Cramton and Katzman state it well: “Bidders submit low bids on products for which the government has overestimated demand and high bids on products where the government has underestimated demand. As a result, prices for individual products do not align with costs, likely resulting in selective fulfillment of customer orders.”

CBP’s final flaw was its long-term roll-out strategy on rural America. As part of the ACA, CMS was mandated to enact CBP pricing to all non-selected MSAs and rural areas across the country by 2016. A non-economist can instinctively point out the flaw here - rural healthcare is simply more expensive to manage. Distance between patients, lack of sufficient healthcare practices, lack of technology access, etc. Thankfully, the 21st Century Cures Act extended this timeline, and enacted a blended rate of CBP and the rural administrative rates for non-MSAs. Given this blended rate is only an interim final rule, it remains to be seen if the blended rate remains the standard for rural non-MSAs going forward.

To be fair, CMS has tried to mitigate these factors (some sooner than others). For one, CMS has always required the lowest bidding suppliers to provide proof that bids are “bona fide” - like Manufacturer Invoices and the like. In response to criticism on the non-binding component, CMS now requires bidders to post a $50,000 bond for each Competitive Bidding Area they are awarded a contract for. Should an awarded bidder abstain from participation, the bidder forfeits the bond to CMS. And most recently, CMS has determined that future bids in CBP will be only lead item in a product category rather than weighted bids for each item in that category. This means that suppliers will only bid on the item in a category that had the most nationally submit charges in the year prior - reducing gaming potential and streamlining administration.

The Results Today

Now that CMS has about a decade of public data on CBP, what has been the market effect? From a CMS savings perspective, CBP has been an objective win. Estimates and studies vary, given inability to control for all variables, but CMS has reported saving of ~35% since the program was initiated in 2011, and estimates that they will achieve savings of $25B within the period of 2013-2022.

However, CBP has had damaging consequences for small businesses. Perhaps most jarringly, nearly 40% of DME suppliers have left the market entirely. From my own anecdotal interviews, small DME suppliers who used to take insurance no longer do, or do so on a very limited basis - decreasing access for those who need equipment and can’t afford to pay largely out of pocket. CMS rate cuts has also spurred mass consolidations, PE roll-ups & acquisitions across the DME industry (see Apria Healthcare, Lincare, AdaptHealth, National Seating & Mobility, etc). Now, I know not everyone in this world is anti-oligopoly, but even granting the potential “net good” of innovative companies like Google and Amazon for consumers, oligopolies built on “ability to comply” rather than service excellence or innovation (aka most healthcare oligopolies) should not get this defense.

Of course, patient access to necessary healthcare service should always be the end-all be-all metric. In this sense, I believe CBP has not been successful. Simply put, CBP design does not account for service, available supply or quality. Sure, there is a quality “minimum” component to CBP, but with no transparency into quality measurement, it’s hard to say whether the minimum is effective or enforced. A price-only focus has fostered a DME supplier patchwork that greatly varies in consistency or quality in the Medicare DME ecosystem. Even finding a DME supplier who is contracted to take a patient’s insurance is a struggle for patients and their caregivers to navigate now, let alone finding a reputable supplier of those.

Variations in supply and quality have harmful downstream effects - especially on long-term health outcomes. Just ask healthcare providers who needed PPE and ventilators in 2020. Long-term costs can be affected too. According to the Council for Quality Respiratory Care, “newly-diagnosed COPD patients who start oxygen therapy within two months of first diagnosis have total health care costs … 20 percent lower than those who start oxygen later.” The same logic applies to people who have delays in receiving walkers, hospital beds, and patient lifts, increasing the risk of falls and thus costly hospital readmissions.

Where Competitive Bidding Stands Today and the Future

The future of CBP is in flux. In the most recent 2021 Rounds, CMS only awarded contracts for two DME items, OTC Kneepads and OTC Braces. Effectively “punting” to the next cycle, CMS stated that the remaining item bids did not result in significant savings for the program. Since the CBP exclusive contracts expired from the previous rounds, any non-participating provider of Medicare (most DME suppliers) can now provide DME supplies at their respective 2017 Round rates. This CBP standstill may have been the result of heavy lobbying by Apria Healthcare (a big DME player) that coincidentally doesn’t sell OTC Knee Braces and OTC Back Braces. Regardless, it remains to be seen what the 2024 CBP Round will look like - or if it even exists.

Should this program continue in the future? There is undoubtedly high value in standardizing prices and reducing costs for Medicare. But if the side effect is less access, lower quality, and higher barriers of entry for suppliers, who really wins? For one, the large supplier incumbents definitely win, with more rules keeping smaller and new players out to play by. Do patients win? As discussed above, I don’t think so. Do small, good-faith DME suppliers win? If they do, it’s by catering to the cash-pay clientele (aka the rich).

To me, the biggest question is whether or not the Competitive Bidding Program can adopt a more agile design dynamic going forward. Will future rounds of CBP modify the rules on median pricing? Will Competitive Bidding bids be allowed to go up over time - to account for inflation at the very least? How does CMS account for the issues in access CBP presents? After all, as current Harvard scholar Yunan Ji notes in her working paper on the subject - “the marginal patient rationed out of DME under competitive bidding … is older, less likely to be white, and more likely to be on Medicaid.” These questions have been deferred for at least the next few years - but it would be a pleasant surprise if the next round of CBP incorporates some of the external criticism and focuses more holistically on patient value instead of strictly lower costs.

Hope you enjoyed the piece! Next time, I will cover and track the growth of some of the largest players in the industry. Fun stuff…stay tuned.